In the Indian Constitution, nowhere the founding fathers have mentioned the word " Budget". The word which they have used for budget is "Annual Financial Statement". The Art-112 of Constitution provides for all the provisions to enact a Annual Financial Statement.

The Annual Financial Statement is the estimated receipts and expenditure of the Government of India in a financial year, which begins on 1st April and ends on 31 st March of the following year.

The Budget has the following elements included.,

1. Estimates of Revenue and Capital receipts

2. ways and Means to raise revenue.

3. Details of Estimates of expenditure.

4. Details of the actual receipts and expenditure of the closing financial year and the reason for any deficit or surplus in that year, and

5. Economic and Financial policy of the coming year, that is taxation proposals, prospects of revenue, spending programme and introduction of new schemes/ Projects.

Separation of Railways Budget:

The central Government of India maintains the Railway Budget and the General Budget separately. The Railway Budget consists of estimates of receipts and expenditure of Ministry of Railway only. But the Union budget consists of the estimates of receipts and expenditure of all the Ministries of the Government of India.

The Railway Budget was separated from the General Budget in 1921 on the recommendations of the Acworth Committee. The reasons are as follows.,

1. To introduce flexibility in railway finance

2. To facilitate a business approach to the railway policy

3. To secure stability of the general revenues by providing an assured annual contribution from railway revenues.

4. To enable the railways to keep their profits a fixed annual contribution to the general revenues.

Stages In Enactment:

1. Presentation Of Budget:

The Annual Financial Statement is presented on the last working day of February. The finance Minister presents the General Budget with a speech known as the " Budget Speech". At the end of the speech in Lok Sabha, the budget is laid before the Rajya sabha in which the members can only discuss it but has no power to vote on the demands for grants or resend the Bill for reconsideration of the President.

2. General Discussion:

The general discussion on Budget begins a few days after its presentation. It takes places in both the houses of Parliament and lasts for three to four days. In this stage, the Lok Sabha can discuss the budget as a whole or on any question of principle involved therein but no cut motion can be moved nor can the budget be submitted to the vote of the House. The finance minister has the general right of reply at the end of the discussion.

3. Scrutiny by the Departmental Standing Committees:

After the general discussion on the annual financial statement is over, the House are adjourned for about three to four weeks. During this period of time, 17 standing committees of Parliament thoroughly examines and discuss in detail about the demands for grants of the related Ministries. Then it prepares reports on them. These reports are submitted to both the houses of Parliament for consideration. It is a inbound financial control over the administration in the country.

4. Voting on Demands for Grants:

After the report is submitted by the Standing Committees, the Lok Sabha takes up the voting process of demands for grants proposed on the scrutinized light of the report. The demands are presented ministry wise . The demands become a grant after it has been duly voted. The sole power to vote on grants are vested in the hands of Lok sabha only. More, the voting is confined to the votable part of the budget. It means , the expenditure charged on the consolidated fund of India is not submitted to the vote but rather it is only discussed.

When the Budget is voted, the members can even discuss the details of the budget. They can also move motions to reduce any demand for grant. Such motions are called as "Cut Motion".

i) Cut Motion: By using this the members can disapprove the policy underlying the demands. It states that the amount of the demand be reduced to Re.1. The members can also advocated an alternative policy.

ii) Economy Cut Motion: It shows the Eco0nomy that can be affected in the proposed expenditure. It states that the amount of the demand be reduced by a specified amount. This could be a lumpsum reduction in the demand or ommission or reduction of an item in the demand.

iii) Token Cut Motion: It mirrors a specific grievances that is within the sphere of responsibility of the Government of the demand be reduced by Rs.100. This motion represents two purposes., 1. Facilitating the initiation of concerned discussion on a specific demand for grant and 2. Upholding the principle of responsible government by probing the activities of the government.

Totally, there are 26 days are allocated for the voting of demands. On the last days the speaker puts all the remaining demands to vote and disposes those demands whether they have been discussed or not . This process is know as " Guillotine". This is also criticized as the Erosion on the Constitution of India.

5. Passing Of Appropriate Bill:

As per the Constitution of India, No Money can be withdrawn from the Consolidated fund of India except under "Appropriation Made By Law". In order to appropriate the fund from the Consolidated Fund Of India, the Appropriation Bill is introduced in the session to meet the required money of 1) Grants voted by Lok Sabha and 2) Expenditure charged on the consolidated fund of India.

In fact, no any amendments can be proposed to the appropriation bill in either house of the parliament that will have the effect of varying the amount or altering the destination of any grants voted or varying the amount of any expenditure charged on the consolidated fund of India. The appropriation bill becomes Appropriation Act after it is assented by the President. Now only the payment is authorized or legalized to withdraw money from the Consolidated fund.

6. Passing Of Finance Bill:

The finance bill as a finance proposal of the Government of India for the following year, it is subjected to all the conditions of a money bill(Art-110). Unlike in Appropriation Bill, the amendments that seeks to reject or reduce a tax) can be moved in the case of finance bill. According to the Collection of Taxes Act of 1931, the Finance Bill must be enacted within 75 days. Now, the Finance Bill of that year legalizes the income side of the budget and complete the process of enacting the Budget.

Finance Commission Of India:

Finance Commission of India is formed by the Art-280 of Indian Constitutional as a quasi judicial body of planning or staff agency. This is formed by the President of India once in 5 years or at such earlier time as he/she considers necessary for the purpose of devolution of non-plan resources.

Composition Of Finance Commission:

The Commission consists of One Chairman and Four other members who are appointed by the President Of India. The parliament is given the power to determine the qualifications of the Members.

Functions of Finance Commission Of India:

1. The Distribution of the net proceeds of Taxes to be shared between the center and states and the allocation between the states of the respective shares of such proceeds.

2. The Principles that should govern the grants in aid to the states by the Center.

3. The measures needed to augment the consolidated fund of a state to supplement the resources of the Panchayats and the municipalities in the states on the basis of the recommendations made by the state finance commission.

4. Any other matter referred to it by the president in the interests of sound finance.

5. The Commission submits its report to the president. He lays it before both the houses of Parliament along with an explanatory memorandum as to the action taken on its recommendations.

6. The advise made by the Commission are advisory only in nature but not binding on the government. It is up to the Union Government to implement its recommendations on granting money to the states.

Qualifications of the Members:

The Chairman shall be a person with experience in public affairs, and the four other members shall be selected as follows.,

1.Have been, or are qualified to be appointed as Judges of a High Court or

2.Have special knowledge of the finances and accounts of Government or

3.Have wide experience in financial matters and in administration or

4.Have special knowledge of economics

On the Following Basis a member is disqualified:

1.Unsound mind

2.Undischarged debts

3.Convicted of an offense involving moral turpitude

4.Financial or other interest as is likely to be prejudicial to his functions

The Finance Commissions Of India Formed so far and so far appointed Chairmans:

What is Measuring National Income:

Measures of national income and output are used in economics to estimate total economic activity in a country or region, including gross domestic product (GDP), gross national product (GNP), and net national income (NNI). In nutshell it is a measure how much output, spending and income has been generated in a given time period.

Methods:

1. Output Method:The total value of the output of goods and services produced in India. It is finding the total output of a nation by directly finding the total value of all goods and services a nation produces. In this method only the final value of a good or service is included in total output.

2. Income Method: The total income generated through production of goods and services. It is finding the total output of a nation by finding the total income received by the factors of production owned by that nation.

3. Expenditure Method:The total amount of expenditure taking place in the economy. It is finding the total output of a nation by finding the total amount of money spent. GDP = C + I + G + (X - M).

National Income:

" A National Income estimate measures the volume of commodities and services turned out during a given period counted without duplication." Thus National Income measures the net value of goods and services in the country.The following are the importance of Calculating National Income.,

- To see the economic development of the country.

- To assess the developmental objectives.

- To know the contribution of the various sectors to National Income.

Concept Of National Income:

The following are the various concepts of National Income.,

1. Cross National Product(GDP):

It refers to the money value of total output or production of final goods and services produced by the nation of a country during a given period of time say for example 1 Year. From this definition let us find the calculation of GNP.,

GNP = Money Value of total output or production of final goods and services produced.

= GDP + (X-M) where GDP = Total money value of all Goods and services produced

within the boundaries of the nation(C+I+G).

so, = Consumer spending(C) + Investments on Assets(I) + Government Spending(G) +(

X(Income earned and received by nationals within boundaries) - M(Money paid by

India or Income received by Other nationals from the country))

= GNP

As GNP stands for Gross figure of national income in must include all the capital investments(GDP) and also revenue incomes(X) and the relevant revenue payments too to be deducted out of the total figure of GDP and X. Now the Gross figure of national income is derived.

Net National Product:

Net National Product is a mostly Revenue nature of Income which will show the net income after the expenses and losses on the capital goods.

NNP = GNP - Depreciation on Capital Stock Consumption

National Income:

Now, let us calculate National Income.,

National Income = NNP - Net Indirect Taxes

= NNP - (Indirect Taxes - Subsidies)

= National Income.

The National Income above derived is nothing but NNP only, but after the above calculation the NNP is at its Factor cost. Before the calculation it is at Market Cost. When NNP is derived at Factor Cost then it becomes National Income.

Public Debt:

It is an instrument of resource mobilization by the modern government. It simply denotes the "Borrowing of Government from People, RBI, Financial Institutions and so on". The following are the classification of Public Debt.,

1. Internal Debt:

When government borrows within the country, it is called internal debt such as borrowings from individuals, business establishments, financial institutions, commercial banks and central bank. Internal debt also includes Loans raised by the government in the open market through treasury bills and special securities issued to the RBI, Rupee securities(non-interest bearing) issued to international such as the IMF and the world Bank and most importantly various bonds like the oil bonds and fertilizer bonds ect.,

2. External Debt:

When government borrows the money from out side the country it is known as External Debt such as borrowings from Foreigners, foreign Banks, Foreign governments and international institutions. Unless the internal debt, the External debt has material loss to the debt country. The following are the some of examples.,

* Long term external debt which is the bulk part

* NRI deposit and multilateral loans

* Commercial borrowings

* Bilateral loans and

* Negligible amount from Export Credit

3. Voluntary and Compulsory:

When the Government borrows by issuing securities to which people are free to subscribe, it is called voluntary debt. When the government on the other hand, enforces borrowing through legal contexts or compulsions , then it is Compulsory debt.

4. Productive and Unproductive:

Productive debt is one which is incurred for those projects which yields income to the government. For example the debt incurred to meet expenditure on power projects, irrigation, public enterprises an railways. Whereas Unproductive debt neither yields any income not creates any assets. Debts incurred for Budgetary deficit, war, natural calamities ect.,

5. Funded and Non-Funded:

Funded debt is a long term debt payable after a year, while unfunded debt is a short term debt, payable within one year.

6. Redeemable and Irredeemable:

When the government borrows the money with a promise to pay off in future at a specified date then it is Redeemable debt. Whereas the government has no such agreement to redeem the money in future then it is irredeemable debt.

Zero Based Budgeting - An Introduction:

ZBB originated and developed in the USA. It was created by Peter A.Phyrr, a management private industry. The then President Jimmy Carter introduced this Budgeting system in USA.

ZBB is a rational system of Budgeting. Under this system, every schemes should be reviewed critically and readjusted totally from Zero)or scratch) before being included in budget. Thus the ZBB involves a total reexamination of all schemes afresh (from base Zero) instead of following the incremental approach to budgeting which begins with the estimation of current expenditure.

Advantages of ZBB:

1. It eliminates the low or lesser prioritized programs.

2. Improves the program effectiveness dramatically.

3. Makes the high impact programs to obtain more finances.

4. reduces the Tax increase.

5. It facilitates critical review of schemes in terms of their cost-effectiveness and cost benefits.

6. It provides for quick budget adjustments during the year.

7. Allocates the scarce resources rationally

8. It increases the participation of line hierarchy bureaucrats in the preparation of budget.

9. It detects Inflated Budget

10. It increases the responsibility in financial decision making in a greater extent.

11. Identifies the absolute source for outsourcing.

12. In India it was introduced in the Department of Science and Technology in 1983 and in all other departments in 1986-87.

13. It is also regarded as a greater legislative control over the executives.

14. Maharashtra government renamed and used it as Development based budget.

What is Fiscal Policy:

It is the use of government expenditure and revenue collection that directly and indirectly influences the economy of the nation. The following are the features of the Fiscal Policy.,

1. It can be contrasted with the other main types of economic policy, monetary policy, which attempts to stabilize the economy by controlling interest rates and supply of money.

2. The Two main instruments used in Fiscal Policy is i) Government spending and ii) Taxation.

3. It refers to the over all effect if the budget outcome on economic activity. In regards with this following are the three stances of Fiscal Policy.,

Fiscal system deals not only with the quantity but the quality of public finance as well. In other words, not merely how much is raised and spent but how has it been raised in the form of

i) Taxes -- Within Direct and Indirect Taxes

ii) Disinvestment proceeds.

iii) Borrowing from market and RBIThe Following are the Instruments are traded in Indian Money Market:

1.Call Money:The money market is a market for short-term financial assets that are close substitutesof money. The most important feature of a money market instrument is that it is liquid and can be turned over quickly at low cost and provides an avenue for equilibrating the short-term surplus funds of lenders and the requirements of borrowers. The call/notice money market forms an important segment of the Indian money market.

2. Commercial Papers:Commercial Paper is short-term loan that is issued by a corporation use for financing accounts receivable and inventories. Commercial Papers have higher denominations as compared to the Treasury Bills and the Certificate of Deposit. The maturity period of Commercial Papers are a maximum of 9 months.

3. Treasury Bills: The Treasury bills are short-term money market instrument that mature in a year or less than that. The purchase price is less than the face value. They have 3-month, 6-month and 1-year maturity periods.The security attached to the treasury bills comes at the cost of very low returns. Treasury bills began being issued by the Indian government in 1917.

4. Commercial Bills: It enhances he liability to make payment in a fixed date when goods are bought on credit through a short term, negotiable, and self-liquidating instrument with low risk.

It may be a demand bill or a usance bill. A demand bill is payable on demand, that is immediately at sight or on presentation by the drawee. A usance bill is payable after a specified time.

5. Certificate Of Deposit: The certificates of deposit are basically time deposits that are issued by the commercial banks with maturity periods ranging from 3 months to five years.The bearer of a certificate of deposit receives interest. The maturity date, fixed rate of interest and a fixed value - are the three components of a certificate of deposit. It was in 1989 that the certificate of deposit was first brought into the Indian money market.

6. Repo Instrument: The Repo or the repurchase agreement is used by the government security holder when he sells the security to a lender and promises to repurchase from him overnight. Repo transactions are allowed only among RBI-approved securities like state and central government securities, T-bills, PSU bonds, FI bonds and corporate bonds.

7. Banker Acceptance: It is a short-term credit investment. It is guaranteed by a bank to make payments. The Banker's Acceptance is traded in the Secondary market. 90 days is the usual term for these instruments. The term for these instruments can also vary between 30 and 180 days.

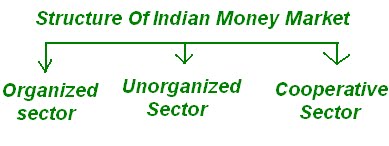

Structure Of Indian Money Market:

The Main Classification Of Indian Money Market:

1.Organized Sector Of Indian Money Market:

2.Unorganized Sector:

3. Cooperative Sector: 1. Call Money Market:

1. Call Money Market:

* The rate in this market is "Call money Rate"

* The market for extreme short period of loans

* Money at call and short notice is primary tool.

* rate is determined by Demand and supply

* Money is lent to Money Brokers and stock exchange dealers.

The most important feature of a money market instrument is that it is liquid and can be turned over quickly at low cost and provides an avenue for equilibrating the short-term surplus funds of lenders and the requirements of borrowers. The call/notice money market forms an important segment of the Indian money market. Under call money market, funds are transacted on overnight basis and under notice money market, funds are transacted for the period between 2 days and 14 days.

2. Acceptance Market:

*Conditional transactions in which a good or service satisfies the needs and demands of a sufficiently large number of customers to continue or increase its production or availability.

* Acceptance of Trade Bills are main theme.

* The main operators are " Acceptance Houses and Commercial Banks"

* Promotes the operations of Discount Bills.

3. The Bill Market:

* The market where the commercial papers are transacted into money or notional money transactions.

* Market that deals for short term papers or bills., say for 6 months or extended.

* Main activity is buying and selling Short term papers and bill that have commercial transactions already done.

* It also includes the Commercial money market transactions and Treasury Bill market which are directly and indirectly connected with Commercial Banks and Acceptance houses.

4. Collateral Loan Market:

* The market where the asset which can be pledged as a security to the creditor by the borrower.

* All the assets to be made securities are transacted in the terms of monetary papers.

* It is very important section of money market in which the capital money and money value of the assets are brought into account. So, it fetches a heavy cash bunch and heavy cash picture both in monetary flow.

* It takes the form of loans over draft, cash credits ect.,

* The loans and advances are covered by collaborates like government securities, gold silver, stock and merchandises.

Money Market - Meaning by RBI:

" Money Market is the center for dealing mainly of short term character, in money assets, it meets short term requirements of borrowers and provide liquidity or cash to the lenders".

The Followings are the Components of Money Market(money channel that distributes the Money):

1. Central Bank : By regulating all the money flows in all the channels and institutions.

2. Commercial Banks: main nodal points for distributing and redistributing the money through various rates of transactions(CRR, SLR, Repo, Reverse Repo and ect.,)

3. Discount House : the institutions that rediscount all the Bills of Exchange.

4. Acceptance House:They are merchant bankers who accept the Bills of Exchange. They act as a second signatory of the bills of exchange.

5. Bill Brokers: They know their customers and act as intermediaries between the sellers and buyers of bill for a small commission.

Credit Control of RBI(briefly)

Need:

1.To encourage the priority sectors for overall growth

2.Fecilitate the flow of adequate volume of bank credit to its industry, agriculture and trade

3.To keep Inflation pressure under check

4.To ensure that Credit is not diverted to undesirable purposes

5.To fecilitate the Development of Indian economic growth

Types of credit control :

1)Quantitative Method

1.Bank rate policy: by controlling the ways and means advances to the govt.

2.Open Market operation: by controling Short term liquidity in the market.

3.variation of cash reserve ratio: by increasing or reducing CRR or SLR.

4.fixation of lending rate: control by Increasing or reducing the rate of primary or secondary lending rates

5.Credit sequeenze: by controlling the amount of bank credit at a certain limit and fixing maximum limit for commercial borrowings.

2)Qualitative Method

1.Fixation of Margin Requirement

2.Regulation of consumer credit

3.Rationing of credit

4.Prior authorisation of schemes

5.Moral sausion

6.Direct Action

RBI - Reserve Bank Of India:

Establishment:The Reserve Bank of India was established on April 1, 1935 in accordance with the provisions of the Reserve Bank of India Act, 1934.

The Central Office of the Reserve Bank was initially established in Calcutta but was permanently moved to Mumbai in 1937. The Central Office is where the Governor sits and where policies are formulated.

Though originally privately owned, since nationalisation in 1949, the Reserve Bank is fully owned by the Government of India.

Functions Of RBI in brief:

Fuctions:

The fuctions are classified into three heads,viz.,

A) Traditional functions

B) Promotional functions and

C) Supervisory functions. lets see the detailed accont in these heads.,A) Traditional functions

1.Monopoly of currency notes issue

2.Banker to the Government(both the central and state)

3.Agent and advisor to the Government

4.Banker to the bankers

5.Acts as the clearing house of the country

6.Lender of the last resort

7.Custodian of the foreign exchange reserves

8.Maintaining the external value of domestic currency

9.Controller of forex and credit

10.Ensures the internal value of the currency

11.Publishes the Economic statistical data

12.Fight against economic crisis and ensures stability of Indian economy.

B) Promotional functions

1.Promotion of banking habit and expansion of banking systems.

2.Provides refinance for export promotion

3.Expansion of the facilities for the provision of the agricultural credit through NABARD

4.Extension of the facilities for the small scale industries

5.Helping the Co-operative sectors.

6.Prescribe the minimum statutory requirement.

7.Innovating the new banking business transactions.

C) Supervisory functions

1.Granting licence to Banks.

2.Inspects and makes enquiry or determine position in respect of matters under various sections of RBI

and Banking regulations3.Implements Deposit insurence scheme

4.Periodical review of the work of the commercial banks

5.Giving directives to commercial banks

6.Control the non-banking finance corporation

7.Ensuring the health of financial system through on-site and off-site verification.

These are all the functions which are protective to the Indian Economy, thats why RBI is considered as the head of all banks.

Structure Of Indian Banking:

1.Scheduled Banks:

Scheduled banks in India constitute those banks which have been included in the Second Schedule of Reserve Bank of India(RBI) Act, 1934. RBI in turn includes only those banks in this schedule which satisfy the criteria laid down vide section 42 (6) (a) of the Act. In 1999, there were 300 scheduled banks in India having a total network of 64,918 branches. The scheduled commercial banks in India comprise of State bank of India and its associates, nationalised banks , foreign banks , private sector banks , co-operative banks and regional rural banks.

2. Non-Scheduled Banks:

Non-scheduled bank in India" means a banking company as defined in clause (c) of section 5 of the Banking Regulation Act, 1949 (10 of 1949), which is not a scheduled bank.

3. Regional Rural Bank(RRBs):

State Bank Of India has the directive control over the RRBs which has spread in 13 states across the country. Till date in rural banking in India, there are 14,475 rural banks in the country of which 2126 (91%) are located in remote rural areas. The main purpose of the RRBs is to develop the rural growth and employment. The Following are the main RRBs presently located in some states.,

1) Andhra Pradesh:

*Andhra Pradesh Grameena Vikas Bank

*Andhra Pragathi Grameena Bank

*Deccan Grameena Bank

*Chaitanya Godavari Grameena Bank

*Saptagiri Grameena Bank

2) Bihar:

*Madhya Bihar Gramin Bank

*Bihar Kshetriya Gramin Bank

*Uttar Bihar Kshetriya Gramin Bank

*Kosi Kshetriya Gramin Bank

*Samastipur Kshetriya Gramin Bank

3) Chattisgarh:

*Chhattisgarh Gramin Bank

*Surguja Kshetriya Gramin Bank

*Durg-Rajnandgaon Gramin Bank

4) Gujarat:

*Dena Gujarat Gramin Bank

*Baroda Gujarat Gramin Bank

*Saurashtra Gramin Bank

5) Haryana:

*Harayana Gramin Bank

*Gurgaon Gramin Bank

6) Himachal Pradesh:

*Himachal Gramin Bank

*Parvatiya Gramin Bank

7) Jammu and Kashmir:

*Jammu Rural Bank

*Ellaquai Dehati Bank

*Kamraz Rural Bank

8) Punjab:

*Punjab Gramin Bank

*Faridkot-Bhatinda Kshetriya Gramin Bank

*Malwa Gramin Bank

9) Assam:

*Assam Gramin Vikash Bank

*Langpi Dehangi Rural Bank

10) kerala:

*Narmada Malwa Gramin Bank

*North Malabar Gramin Bank

11) Jharkand:

*Jharkhand Gramin Bank

*Vananchal Gramin Bank

12) Tamil Nadu:

*Pandyan Grama Bank

*Pallavan Grama Bank

13) Mahdya Pradesh:

*Narmada Malwa Gramin Bank

*Satpura Kshetriya Gramin Bank

*Madhya Bharath Gramin Bank

*Chambal-Gwalior Kshetriya Gramin Bank

*Rewa-Sidhi Gramin Bank

*Sharda Gramin Bank

*Ratlam- Mandsaur Kshetriya Gramin Bank

*Vidisha Bhopal Kshetriya Gramin Bank

*Mahakaushal Kshetriya Gramin Bank

*Jhabua Dhar Kshetriya Gramin Bank

14) Maharashtra:

*Marathwada Gramin Bank

*Aurangabad -Jalna Gramin Bank

*Wainganga Kshetriya Gramin Bank

*Vidharbha Kshetriya Gramin Bank

*Solapur Gramin Bank

*Thane Gramin Bank

*Ratnagiri-Sindhudurg Gramin Bank

15) Karnataka:

*Karnataka Vikas Grameena Bank

*Pragathi Gramin Bank

*Cauvery Kalpatharu Grameena Bank

*Krishna Grameena Bank

*Chikmagalur-Kodagu Grameena Bank

*Visveshvaraya Gramin Bank

16) Rajasthan:

*Baroda Rajasthan Gramin Bank

*Marwar Ganganagar Bikaner Gramin Bank

*Rajasthan Gramin Bank

*Jaipur Thar Gramin Bank

*Hodoti Kshetriya Gramin Bank

*Mewar Anchalik Gramin Bank

17) Orissa:

*Kalinga Gramya Bank

*Utkal Gramya Bank

*Baitarani Gramya Bank

*Neelachal Gramya Bank

*Rushikulya Gramya Bank

18) West Bengal:

*Bangiya Gramin Vikash Bank

*Paschim Banga Gramin Bank

*Uttar Banga Kshetriya Gramin Bank

19) Meghalaya:

Ka Bank Nogkyndong Ri Khasi- Jaintia

20) Arunachal Pradesh:

Arunachal Pradesh Rural Bank

21) Nagaland:

Nagaland Rural Bank

22) Manipur:

Manipur Rural Bank

23) Tripura:

Tripura Gramin Bank

24) Mizoram:

Mizoram Rural Bank

25) Uttar Pradesh:

*Purvanchal Gramin Bank

*Kashi Gomti Samyut Gramin Bank

*Uttar Pradesh Gramin Bank

*Shreyas Gramin Bank

*Lucknow Kshetriya Gramin Bank

*Ballia Kshetriya Gramin Bank

*Triveni Kshetriya Gramin Bank

*Aryavart Gramin Bank

*Kisan Gramin Bank

*Kshetriya Kisan Gramin Bank

*Etawah Kshetriya Gramin Bank

*Rani Laxmi Bai Kshetriya Gramin Bank

*Baroda Western Uttar Pradesh Gramin Bank

*Devipatan Kshetriya Gramin Bank

*Prathama Bank

*Baroda Eastern Uttar Pradesh Gramin Bank

26) Uttaranchal :

*Uttaranchal Gramin Bank

*Nainital Almora Kshetriya Gramin Bank

{kind=link}

Banks In India:

Nationalization Of Banks:

Nationalization of Banks in 1969 has been one of the significant economic, political and social events of Post Independent India. Apart from the fact that it had the imprint of the personality of Mrs. Indira Gandhi, it has several significances which merit attention. The Indian banking industry had become an important tool to facilitate the development of the Indian economy during this time. Jayaprakash Narayan, a national leader of India, described the step as a "masterstroke of political sagacity." Within two weeks of the issue of the ordinance, the Parliament passed the Banking Companies (Acquisition and Transfer of Undertaking) Bill, and it received the presidential approval on 9 August 1969.

Reasons for Nationalization:

1. Reasons by the then PM Smt.Indira Gandhi:

1. The removal of unnecessary control over money flow

2. For adequate credit facilities to agriculture, small industry and exports

3. Professional bent to Bank Management

4. Encourage Entrepreneurial Development

5. Adequate training and terms for banking staff.

2. Monetization of government transactions for the purpose of welfare state.

3. Overall Monetary Integrations.

4. Socialization of issues of Government for the purpose of welfare activities.

5. Preventing concentration of economic powers.

6. Giving social control over monetary behaviors.

7. Channeling for planning and priority sectors.

8. Greater mobilization of funds.

9. Greater agricultural concentration.

10. balanced regional development.

11. Greater control by central Bank(RBI).

12. Small stake of shareholders.

13. Greater stability of Banking structure.

14. Greater socialism activities.

15. Better service conditions to staffs.

16. New schemes to be implemented easily.

The Nationalized Banks in India:

*Nationalised Banks

* Allahabad Bank

* Andhra Bank

* Bank of Baroda

* Bank of India

* Bank of Maharashtra

* Canara Bank

* Central Bank of India

* Corporation Bank

* Dena Bank

* Indian Bank

* Indian Overseas Bank

* Oriental Bank of Commerce (OBC)

* Punjab and Sind Bank

* Punjab National Bank (PNB)

* Syndicate Bank

* UCO Bank

* Union Bank of India

* United Bank of India (UBI)

* Vijaya Bank

State Bank of India and Associates

* State Bank of India (SBI)

* State Bank of Bikaner and Jaipur (SBBJ)

* State Bank of Hyderabad (SBH)

* State Bank of Indore (SBIR)

* State Bank of Mysore (SBM)

* State Bank of Patiala (SBP)

* State Bank of Saurashtra (SBS)

* State Bank of Travancore (SBT)

Other Public Sector Bank

* IDBI Ltd.

Various Committees On Taxation Reforms In India:

1. Taxation Enquiry Committee:

i) It was established in 1953 chaired by Dr.John Mathal.

ii) To examine the incidents of Central, State and Local taxation on various classes of people.

iii) To examine the suitability of tax system to remove inequalities.

iv) To examine the effect of taxation on income and capital formation.

v) To explore fresh avenues of taxation

2. Indian Tax Reforms Committee:

i) Made in 1956

ii) Chaired by Prof.Kaldor

iii) Measures to widen the basis of Taxation on the following items.,

* Wealth Tax

* Capital Gains Tax

* Gift Tax

* Expenditure Tax

* Reforming

* Commercial Tax

* Tax Evasion

3. Boothalingam Committee:

i) main report was on " Rationalization and Simplification of Direct Taxation in India.

ii) Recommended 10% advalorem on all products.

iii) Simplification of Customs rates.

iv) Raising of exemption limit to the Income tax.

v) Abolition of Dividend Tax.

4. Direct Taxes Enquiry Committee:

i) Made in 1970 and Chaired by Mr.K.N.Wanchoo.

ii) Main concern of the committee was on Black Money.

iii) Extent of Black Money

iv) Causes of Tax Evasion

v) Measures to unearth Black Money

vi) Fighting Tax Evasion.

Value Added Tax:

The VAT belongs to the family of Sales Tax(one of the Indirect Taxes). It can be defined as " A Tax to be paid by the manufacturers or traders of goods and services on the basis of value added by them". It is not on the total manufactured or sold products but on the Value added by the manufacturers and producers.

VAT = Tax Base(Value Added by the manufacturers) * rate of tax

Highlights Of VAT:

1. Recommended by Empowered Committee of state Finance Ministers, in its meeting in 2004.

2. Now, all the states have agreed upon VAt and the last state which added VAT was Uttar Pradesh

3. The states level VAT being implemented presently has replaced the Sales tax.

4. Central Government acts as a facilitator to successful implementation of VAT.

5. Rate of Tax mainly is 4% on declared goods or goods commonly used and 10%-12% on goods called revenue neutral rates.

6. Two special rates imposed - 1% on silver or Gold and 20% on liquor.

7. Tax on Petrol, diesel or aviation turbine fuel are proposed to be kept out of from VAT system as they would be continued to be taxed as presently applicable by the CST Act.

8. With out the rate discrimination, VAT provides the Uniform Rates which helps to reduces the tax evasion and black money.

9. Tax concession to new industries is done away with in the VAT system.

10. All the tax paid on the goods purchased within the states would be adjusted against the tax, payable on the sales, whether within the state or in the course of interstate.

11. This helps to avoid the Trade Diversion of any states that has trade transaction with some other states which may have different tax system that may discourage the neighbor states to avoid or deviate such trades with those states.

12. As VAT levies tax on the value added by the producers, it completely avoids the Cascading effect(the tax is levied on the total amount that includes the amount of tax alreday paid in some other different stages of VAT.

Advantages:

1. Easy to Administer

2. Effective and Efficiency

3. Neutrality

4. Reduce Tax Evasion

5. Possibility of Cross Checking

6. Less Tax Burden

7. Encourage Exports.

8. Improved Productivity

9. Burden of Tax is shared by all Factors.

10. Major Source of revenue is possible due to encouraged tax payers.

Disadvantages :

1. Not as simple system to adopt in under developed country

2. Requires an advanced and wide economic structure

3. Possibility of Tax avoidance

4. High cost of maintaining

5. May cause to inflation

6. Regressive nature of operation.

Tax:

Tax is a particular rate of amount or portion of income of the above average income people which will help the functioning of the government for the nation's welfare development. Tax is an important source of Government that plays a vital role in budget corpus and financial management.

Tax System In India:

India has two types of Taxes., namely i) Direct Taxes and ii) Indirect Taxes. India as a semi federal government, all the state governments too have been permitted to levy tax. But the states are restricted in the the sphere of Indirect taxes like Sales Tax, VAT or MODVAT ect., BUT THE SOLE POWER TO LEVY AND COLLECT THE DIRECT TAXES IS FETCHED IN THE HANDS OF CENTRAL GOVERNMENT ONLY. As the quasi federal, Central shares the Direct Taxes collected, with the state governments as "GRANDS IN AID". Apart from that, States and Central governments are allowed to levy and collect Taxes in some classified regards by the Constitution of India. But there are no taxes which are levied by both the Governments after 80th Constitutional amendments.

Tax Income Sharing between Center and States:

1. Art-268A - Service Taxes levied by Union and collected and appropriated by Union and states.

2. Art-269 - Taxes levied and collected by Union but assigned to the States.

3. Art-270 - Taxes levied and distributed between Union and States.

4. Art-271 - Surcharges on certain duties and taxes for purpose of the Union

5. Art-272 - Taxes levied and collected by Union and may be distributed between Union and States.

6. Art-273 - Grands in lieu of export duty on jute and jute products.

Direct Taxation In India:

Direct Taxation in India is based on proportional rate system which will be progressive base levied on the Income slab that shows the gradual and relevant progress of the income of the tax payers which gets such progress in accordance with progress of the Indian Economy.

The 2010 and 2011 Tax proposal is an best example for this.,

Up to 1,60,000

Up to 1,90,000 (for women)

Up to 2,40,000 (for resident individual of 65 years or above) - Nil

1,60,001 – 5,00,000 - 10%

5,00,001 – 8,00,000 - 20%

8,00,001 upwards - 30%

Let us see the Types of Direct Taxes one by one.,

1. Tax on Income or Personal Tax:

Personal Tax is levied on the Personal Income gained by the above average income earner which is fixed by the finance ministry. This tax is levied on the income of the individuals , Hindu families, unregistered firms and others associations of peoples. The marginal rate for income tax in India was 97.75% which was the highest in the world. On the direction of the DIRECT TAX ENQUIRY COMMITTEE the marginal rate of tax was reduced to 77%.

2. Corporate Tax:

It is levied on the Income of registered companies and corporations. As the companies are regarded as the separate legal entity, the income of the companies and corporates are also taken as individual income. Like the individual tax provisions, parliament also establishes Corporate Tax too separately.

In India, Zero Tax companies requires handling. This has done by levying a Minimum Alternate Tax(MAT). The current base of MAT is book profits. This is easily manipulates by various companies to generate zero tax.

3. Wealth Tax:

*It is levied on excess of net wealth of an individual or corporate, Joint Hindu Family. For the purpose of assessing the net value of the wealth , the market value is taken as base value.

* Certain wealths like Agricultural lands, Agri assets, Balance of Provident Fund, Life insurance are exempted from the wealth tax .

* Productive assets like share bonds and bank deposits are exempted from wealth tax after the recommendations of Raja Chellaiah committeee.

4. Estate Duty:

It was levied on total property passing on the death of a person. It was abolished in 1985 by Indian Government.

5. Gift Tax:

It was leviable on all donations except the ones given by Charitable institutions, government companies and private companies. It was abolished in 1998.

No comments:

Post a Comment